All

The Concerning State of The Quantum Supply Chains

Quantum computing is no longer a distant scientific curiosity. Governments, defence ministries, and technology companies around the world are racing to deploy quantum systems that promise computational power fundamentally beyond the reach of today's classical computers. Yet, the public conversation has focused almost entirely on quantum bits (qubits), the quantum equivalent of the binary bits that underpin classical computing, and on the algorithms that run on them. This fixation misses a deeper and more immediate challenge: the physical infrastructure required to build, manufacture, and operate quantum hardware at scale.

Quantum technology is a dual-use category, meaning the same hardware, materials, and know-how that enable scientific research and civilian use cases, can also underpin national security applications. This places quantum firmly alongside semiconductors and advanced aerospace technology as a strategic capability that nations are actively working to control, stockpile, or dominate.

Scaling quantum technology is constrained as much by the availability of raw materials, specialised processing, enabling infrastructure, and the policies that govern them as it is by advances in qubit design or software development. The bottlenecks are physical as much as they are computational, and many of them exist upstream of the laboratory, deep in industrial supply chains that have never been designed with quantum security in mind.

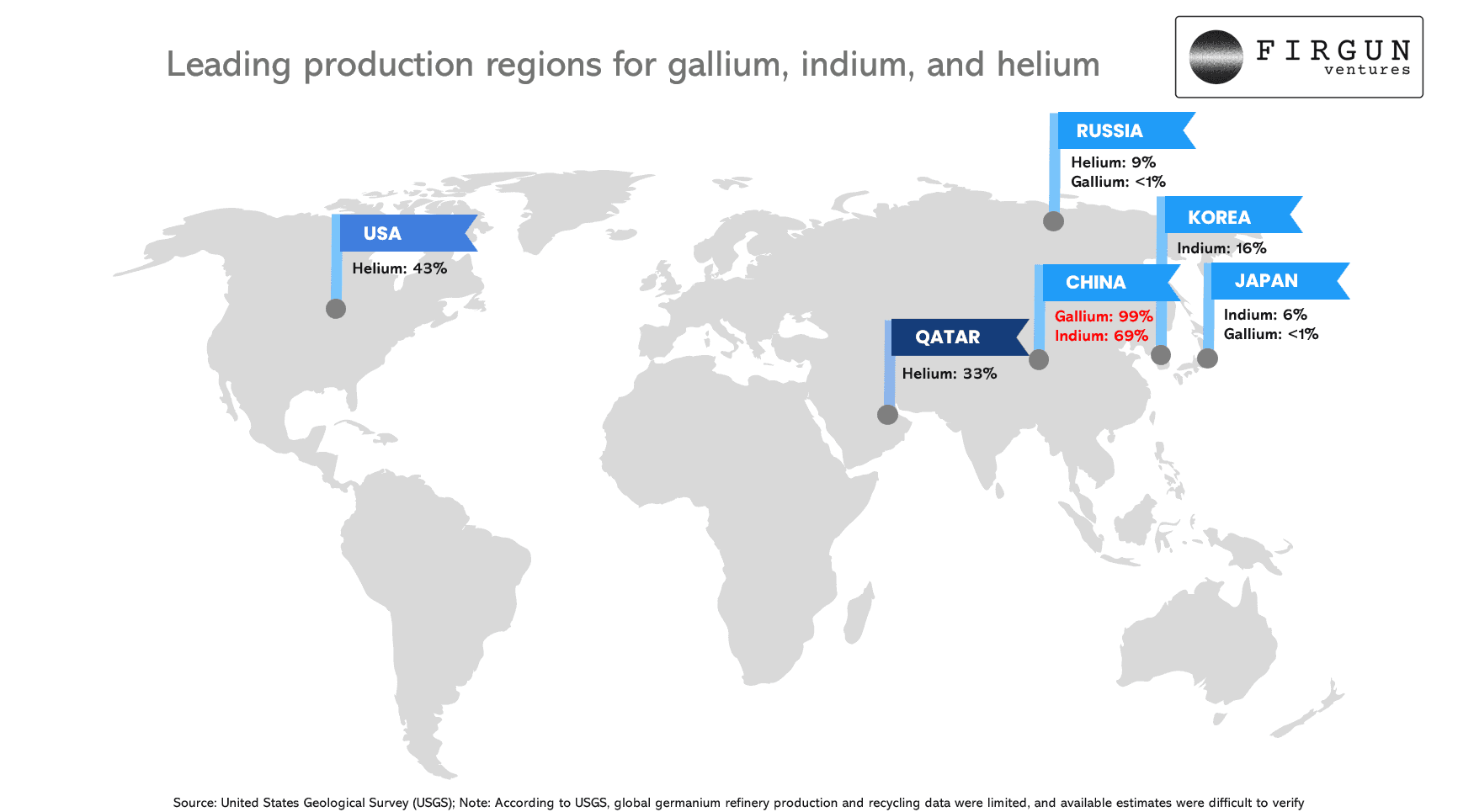

The geopolitical climate sharpens this risk profile considerably. Take, for example, cryogenics and the prerequisite, ultra-cold temperatures achieved through the use of helium. The ongoing conflict involving the United States and Iran across the Middle East has introduced a new vector of supply disruption that bears directly on helium availability. Qatar, the world's second-largest helium producer after the United States, ships the majority of its helium output as liquefied natural gas via the Strait of Hormuz, one of the world's most strategically sensitive maritime chokepoints. Heightened tensions in the region raise the prospect of helium shipment disruption that could tighten an already constrained supply.

This article examines supply chain risk across the five leading (arguably) quantum computing modalities (meaning the different physical modalities of embodying qubits): superconducting qubits, trapped-ions,, neutral atoms, photonic systems, and silicon spin qubit systems, through the lens of raw materials, components, and equipment. The supply chain twist is that these modalities look diverse, but they converge on a surprisingly small set of shared bottlenecks. The goal is not to be alarmist, but rather to paint a picture identifying where the vulnerabilities are, why they exist, and what mitigation paths are plausible.

It is also worth noting at the outset that this article addresses supply chain risk through a materials, components, and infrastructure lens. Talent, the availability of trained quantum engineers, physicists, and technicians, is an equally important bottleneck that this article does not cover, but which deserves serious attention in its own right, particularly as workforce development programmes are scaled back and access to international talent pools becomes more politically contested.

TL;DR

Across the more mature quantum computing modalities, there are a set of overlapping and compounding supply chain vulnerabilities, of which several key themes are emerging.

Export controls and industrial policy represent the first major risk layer. Nations, primarily the United States and China, are actively weaponising access to critical materials and equipment. China's restrictions on gallium and germanium exports, two metals that are essential inputs for lasers, detectors, and semiconductors used in quantum systems, are a live and escalating example. These controls do not target quantum technology directly, rather, they propagate indirectly through the enabling components that every quantum platform depends on.

Depending on your country’s or company’s geopolitical allegiance, processing concentration outside NATO-aligned jurisdictions represents the second risk layer. Even when raw materials are available in principle, the high-purity refining and processing capacity needed to turn them into quantum-grade inputs is heavily concentrated in a small number of countries, many of which are not or not fully strategically aligned with Western interests. This processing chokepoint gives a handful of nations, such as China, substantial leverage over the quantum ambitions of others.

Cryogenic infrastructure is the third major vulnerability. Superconducting quantum computers must operate at temperatures colder than outer space, and the helium-3 isotope required to reach these temperatures is extraordinarily scarce, produced only as a decay product of tritium in nuclear weapons programmes.

Finally, the semiconductor stack functions as a common denominator across modalities. Gallium, germanium, indium, and ultra-pure silicon-28 appear as enabling inputs in almost every quantum platform, whether in the qubit itself, in the lasers that manipulate ions and atoms, or in the classical electronics that read out and control quantum states. This means that diversifying into multiple quantum modalities does not automatically mitigate supply chain risk, especially if they all converge on the same enabling bottlenecks. Hence, concentration risk is not reduced, it is simply obscured.

The strategic implication is clear: quantum readiness is not only a software and algorithm challenge. It is a materials and manufacturing challenge, one that demands urgent, coordinated attention from investors, policymakers, industry and technologists alike.

Theme 1: Export controls and policies of dual-use materials

Assessing supply chain vulnerability

Supply chain vulnerability in quantum technology is typically assessed across three dimensions: criticality (assessing how essential the material or component is to the system), substitutability (ability to be replaced by another mineral or component), and supplier concentration (the number of independent sources which exist).

Quantum systems generally score poorly on all three dimensions across a surprising range of inputs, which was recently summarised in last year’s Critical Vulnerabilities in the Quantum Computing Supply Chain within the NATO Alliance report, and previously in this Stanford’s University policy white paper of 2023, "A Framework for Assessing Vulnerabilities in the Quantum Computing Materials Supply Chain". Many of the materials involved are rare, geologically concentrated, and produced in quantities that were not designed to service a global quantum industry.

How export controls propagate

There are two distinct routes through which export controls affect the quantum supply chain. The first is direct: placing quantum hardware, systems, or software on a controlled list that requires government approval before export. The second route is indirect and more covert, which involves applying controls to the enabling tools, components, and materials needed to build and operate quantum systems, without ever mentioning quantum explicitly.

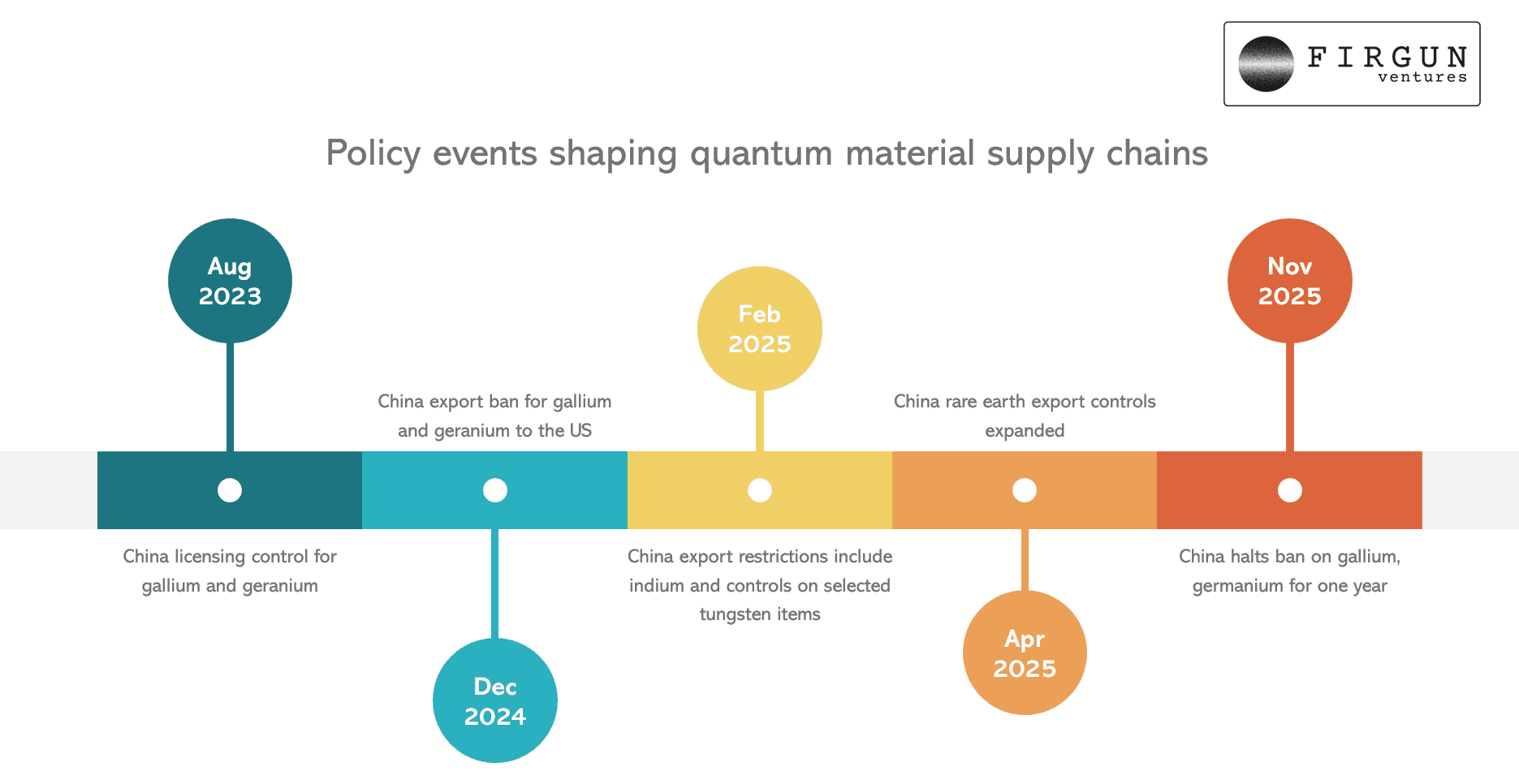

When China restricted exports of gallium and germanium in August 2023 (official ban on US exports in 2024, before being lifted for one year in November 2025), framing the restrictions as a national security measure, quantum hardware developers were caught in the crossfire. Both metals are essential for compound semiconductors (a class of semiconductor made by combining two or more elements) used in the laser systems, photodetectors, and RF (radio frequency) control electronics that are integral to multiple quantum platforms. The restrictions also affect indium, another critical input in the quantum semiconductor stack.

In the Western hemisphere, the United States’ Bureau of Industry and Security implemented Commerce Control List controls for gate-based quantum computers above specific thresholds. The logic explicitly combines scale (34 or more physical qubits) with quality (gate error rates), and it extends beyond the "computer" to include qubit devices, control components, and associated "software" and "technology" for development and production. The United Kingdom, The Netherlands, Spain and Canada have similarly signalled quantum controls in updates to its export control regimes, including listing quantum computers as controlled items and adding related controls that touch semiconductor materials and software relevant to advanced chips.

Regulatory frameworks: Wassenaar, GATT/WTO, and National Quantum Initiatives

Multilateral export control frameworks have attempted to keep pace with quantum's strategic rise. The Wassenaar Arrangement, a voluntary export control regime, originally conceived in the 1990s to adapt to the post-Cold War world, with by now 42 member states, and covering conventional arms and dual-use goods, has been extended to include certain quantum cryptography and sensing technologies. However, Wassenaar is a consensus-based mechanism with limited enforcement authority, and notable non-members, including China, operate outside its scope.

The General Agreement on Tariffs and Trade (GATT) and its successor frameworks under the World Trade Organisation nominally protect against arbitrary trade restrictions, but general (Art. XX) and national security exemptions (Art. XXI), invoked with increasing frequency, have provided legal cover for precisely the kind of targeted export controls now being applied to quantum-adjacent materials.

In response, Western governments have moved to establish affirmative industrial policies. The US National Quantum Initiative, renewed and expanded through the US CHIPS and Science Act (2022), earmarks federal investment for quantum research and supply chain resilience. NATO allies such as UK and Denmark have begun signing memoranda of understanding (MOUs) on quantum cooperation, establishing early frameworks for shared access to quantum infrastructure and materials. The consensus grouping referred to as the US-led Pax Silica Declaration of December 2025, a reference to the semiconductor supply chain alliances forming between the US, EU, Japan, South Korea, and others, is beginning to extend its logic to quantum inputs and build trusted supply chains among partners. These frameworks are nascent and incomplete, but they signal an important shift: governments are beginning to treat quantum supply chain sovereignty as a national security imperative.

The Genesis Mission, signed by President Trump in November 2025, explicitly names quantum information science alongside AI and semiconductors as a priority domain for the Department of Energy's integrated national research platform. Notably, Section 2(b) of the order requires the platform to meet supply chain security standards, a quiet but telling acknowledgement that quantum ambition and hardware sovereignty cannot be separated.

Theme 2: Processing concentration beyond NATO borders

The processing and refinement challenge

It is tempting to believe “if we can mine enough of the raw material, we are safe”. Quantum supply chains punish that assumption because raw material availability is a necessary but insufficient condition for quantum supply chain resilience. The materials must also be refined to extraordinary levels of purity before they become usable in quantum hardware. For most quantum applications, trace contamination measured in parts per billion, the equivalent of a single drop of impurity in an Olympic-sized swimming pool of material, can degrade or destroy quantum performance. The industrial processes required to achieve this level of purity are capital-intensive, technically demanding, and rarely duplicated unnecessarily.

As a result, an estimated 90% of high-purity processing capacity for key quantum inputs sits outside NATO-aligned jurisdictions, driven by the electronics sector showing strong dependence on fabrication facilities within Asia. This is not a malicious arrangement but reflects decades of industrial geography where processing capacity followed cheap energy, skilled labour, and proximity to raw material sources. Even if a Western nation can mine or source the underlying ore, converting it to quantum-grade material may require transiting a single facility or country that sits outside its strategic orbit.

Niobium, tantalum, tungsten, and rare earths

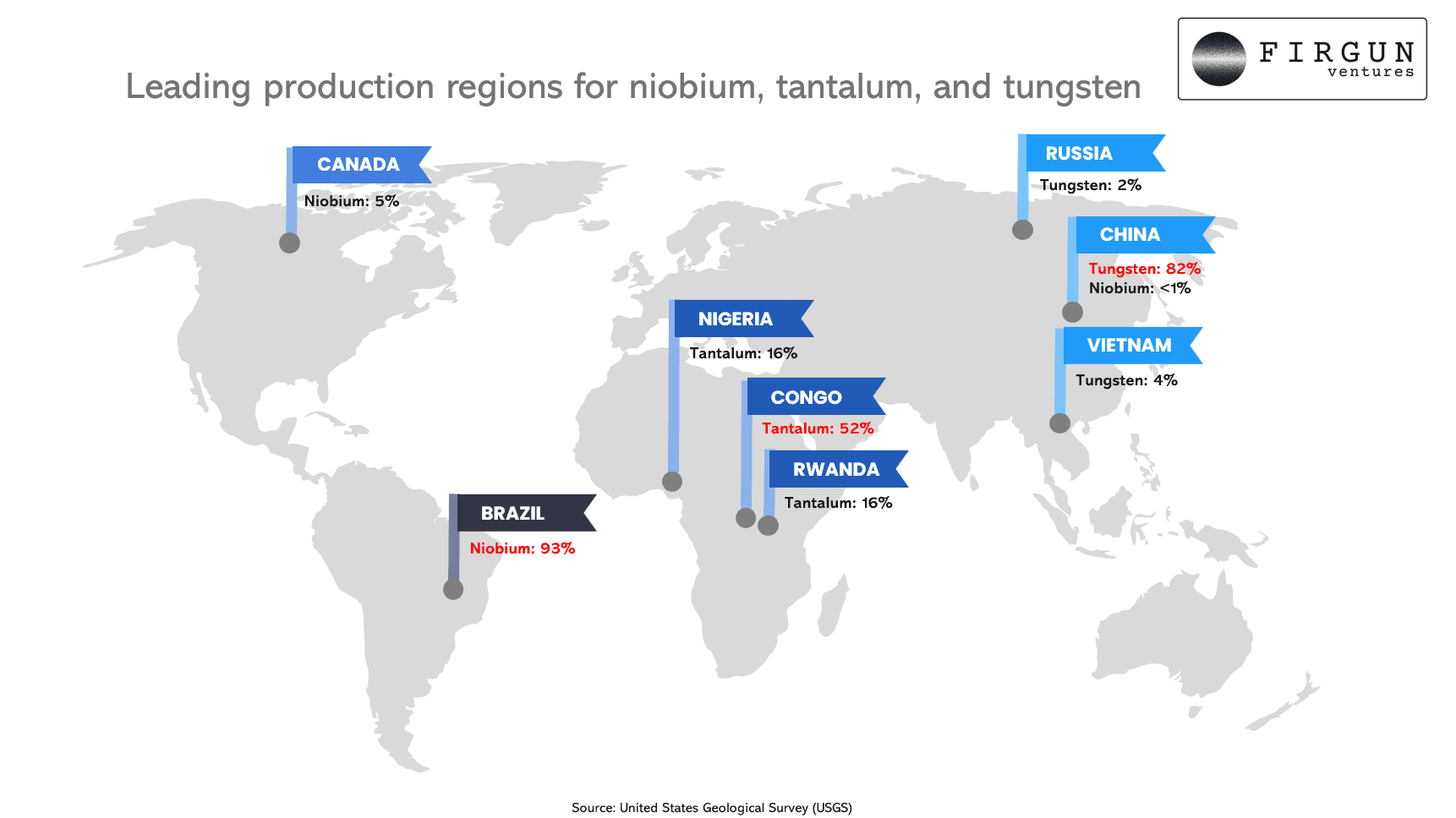

Niobium is the clearest example of both single-country dominance and cross-modality impact. Approximately 93% of global niobium production comes from Brazil, specifically from a small number of mines in the state of Minas Gerais operated by a single company (The Companhia Brasileira de Metalurgia e Mineração (CBMM)). Niobium is the workhorse metal of superconducting quantum computing, as superconducting qubits are typically fabricated from niobium or niobium-titanium alloys, and the microwave resonators and interconnects that support them also depend on the metal. Any disruption to Brazilian niobium supply, whether political, logistical, or geological, would directly constrain superconducting quantum hardware production worldwide.

Tantalum, another refractory metal (meaning it has a very high melting point and is chemically resistant), is used in capacitors and passive components across a wider variety of quantum modalities' classical control electronics. Tungsten appears in connection substrates and chip packaging. Both are subject to supply concentration, and in the case of tungsten, world supply is again dominated by Chinese production, with China producing the majority of mined tungsten. In China’s latest draft of its 5-year plan, the document outlines plans that the central government intends to implement through to 2030, including bolstering its competitive advantages in rare earths. The document highlights Beijing’s focus on prioritising risk mitigation related to the ongoing trading wars, through enabling a more robust response mechanism to enhance its supply chain and security. This could spell further export controls and tightening of rare earth materials, reinforcing the supply chain vulnerabilities facing the West.

In February 2026, Glasgow-based quantum hardware startup, Quantcore, raised £2.5 million to expand UK manufacturing capacity for superconducting quantum computer components. The company is focused specifically on manufacturing niobium-based quantum components, the superconducting building blocks of the most commercially advanced quantum platforms. Quantcore's raise is a small but meaningful data point in a larger story, which is the recognition that quantum hardware sovereignty requires manufacturing sovereignty, and that building this capability domestically, even at a premium, may be strategically necessary for the West.

Theme 3: Cryogenics and the helium-3 bottleneck

The cold dilemma

If superconducting quantum computing had a "main power cable", it would be cryogenics. Superconducting quantum computers must operate at temperatures close to absolute zero, typically around milliKelvin (mK) temperatures just shy of the coldest temperature physically possible, and colder than the average temperature of deep space. At these temperatures, certain metals lose all electrical resistance and enter a superconducting state, enabling the coherent quantum behaviour on which superconducting qubits depend. Achieving and sustaining these temperatures requires a specialised piece of equipment called a dilution refrigerator, which works by mixing two isotopes of helium, helium-3 and helium-4, in a process that absorbs heat from the surrounding environment.

Helium matters in two distinct ways. First, helium is hard to substitute in true cryogenic applications. The United States Geological Survey (USGS) notes there is nothing that substitutes for helium when temperatures below roughly -429 degrees Fahrenheit are required.

Secondly, Helium-4 is relatively abundant and commercially available while Helium-3 suffers a contrasting fate. Helium-3 is produced primarily as a by-product of the radioactive decay of tritium, a hydrogen isotope that is itself produced in nuclear weapons programmes. Global helium-3 supply is therefore intrinsically linked to the pace of nuclear weapons maintenance, and production volumes are small, inelastic, and controlled by a tiny number of state actors, principally the United States and Russia. There is no scalable commercial route to producing more helium-3 quickly, however, Seattle-based company Interlune, has highlighted potential plans to gather scarce Helium-3 from the moon for quantum computing here on Earth.

Dual-use dimensions and supplier concentration

The dilution refrigerators themselves add another layer of concentration risk. The global market for dilution refrigerators is dominated by a very small number of manufacturers, principally Bluefors (Finland), Oxford Instruments (UK), and Leiden Cryogenics (Netherlands). These systems take 6–9 months to manufacture and deliver under normal conditions, and demand has surged considerably as quantum computing programmes have proliferated worldwide. Alongside superconducting quantum computers, photonic quantum systems are also affected, though indirectly. The superconducting nanowire single-photon detectors (SNSPDs), extremely sensitive light detectors used in photonic quantum systems, must operate at cryogenic temperatures (though not as extreme as superconducting qubits), creating their own helium dependency.

A recent and very practical mitigation signal comes from the Dutch Project Quper, as Leiden Cryogenics and Orange Quantum Systems report that their Quper prototype "mini-fridge" aims to cool samples below 25 milliKelvin with reduced reliance on helium-3 and eliminates the need for liquid nitrogen entirely. If successfully scaled, Quper's approach could reduce the cryogenic bottleneck significantly. Lower helium-3 consumption per system means the existing global supply stretches further, and a smaller physical footprint reduces infrastructure requirements, potentially accelerating quantum deployment timelines.

Theme 4: The semiconductor stack: a common denominator

Gallium, germanium, and indium: the enabling trio

Beneath the visible diversity of quantum modalities lies a common substrate: the classical semiconductor stack. Every quantum system, regardless of whether its qubits are formed from superconducting circuits, trapped ions, neutral atoms, or photons, requires classical electronics to control qubit operations, read out results, and process signals. These classical control and read-out systems depend on the same semiconductor materials that underpin modern telecommunications, data centres, and defence electronics.

Gallium and germanium are the most acute examples. Both are produced not as primary mining targets but as by-products of other metal production. Gallium is extracted from bauxite during aluminium refining, and germanium is recovered from zinc smelting. This co-production structure means that supply cannot be easily ramped up in response to demand from quantum programmes alone; it is instead tied to the economics and output of much larger industrial processes. As a stark reminder mentioned earlier, China controls the dominant share of global gallium and germanium processing, which is precisely why its export restrictions in recent years raised alarms across the semiconductor and quantum communities.

Indium, another metal in the same family, is used in indium phosphide (InP), a compound semiconductor that is central to photonic quantum components, high-speed lasers, and photodetectors. Indium phosphide demand is driven primarily by data centre optical interconnects and telecommunications, markets many orders of magnitude larger than the current quantum sector. This means that quantum hardware developers are price-takers in a market shaped by hyperscaler data centre build-outs and AI infrastructure demand, with limited ability to secure preferential access to supply during periods of shortage.

Spin qubits, another leading modality, represent a partial exception to the compound semiconductor dependency, as they can be built on silicon. However, they require silicon enriched to near-perfect purity in the silicon-28 isotope (naturally occurring silicon is a mixture of three isotopes). Silicon-28 is not a mass commodity, and enrichment is an extraordinarily specialised process, with only a handful of facilities worldwide capable of producing it at the required purity levels. Access to silicon-28 supply is therefore another potential chokepoint, albeit one concentrated in a different part of the supply chain.

Conclusion: the supply chain is critical in the future of quantum

Quantum computing's trajectory will be shaped not only by the ingenuity of algorithm designers and the precision of qubit engineers, but by the resilience of the physical supply chains that make quantum hardware possible in the first place. Four main vulnerabilities stand out if you look at quantum technologies through a supply chain lens rather than a qubit lens: export and dual-use control dynamics driven by geopolitical competition, processing concentration outside Western alliances, cryogenic infrastructure with near-irreplaceable inputs, and a semiconductor stack that cuts across every major platform in the field.

In a nutshell, quantum is now firmly in the dual use category, and this is shaping both export controls and industrial policy. Controls increasingly apply to systems, their components, and the software and know-how needed to build them, which means supply chain risk is as much regulatory as it is industrial. Processing and high purity manufacturing are the critical bottlenecks, often outside NATO aligned jurisdictions. Gallium being almost entirely produced in one country at the primary low purity stage, niobium being dominated by a single producer country, and rare earth imports and processing being heavily China exposed are not theoretical risks. They show up as measurable concentration and as observable policy leverage via export restrictions. Cryogenics and industrial gases, especially helium isotopes, can become gating factors for scaling, and they intersect directly with defence-linked supply chains through tritium and helium-3. Meanwhile, the semiconductor and photonics demand curve is so large that quantum will often be competing for inputs rather than driving markets.

None of these vulnerabilities is insurmountable. Helium recycling, alternative dilution refrigerator designs, domestic niobium processing investment, and allied supply chain agreements all represent credible mitigation paths. The emergence of companies like Quantcore in Glasgow and projects such as Quper in the Netherlands demonstrates that founders are taking note and that the private sector is also beginning to price these risks and respond with targeted capital allocation. However, as it stands today, the pace of commercial and policy response remains slower than the pace at which geopolitical pressure is building.

A common instinct among quantum programme managers and investors is to spread risk by supporting multiple modalities, funding both superconducting and photonic programmes, for example, in the hope that their supply chain risks will differ. This instinct is sound in principle but limited in practice. The result is that the supply chain risk profile of a diversified quantum portfolio may look less diversified than it appears on paper. If most or all modalities share the same upstream bottlenecks in gallium, niobium, helium-3, and precision fabrication equipment, then backing all four does not reduce exposure to those bottlenecks, it multiplies it. This convergence effect should be a central consideration for any investor or policymaker designing a quantum resilience strategy.

A balanced call to action is therefore pragmatic. For governments, do map dependencies at the component level, not just the commodity level, and create qualification and standards pathways that make second sourcing realistic. For industry, treat supply chain resiliency as an engineering requirement and a commercial requirement, which means designing for lower scarce-input usage, building test infrastructure to reduce iteration delays, and investing early in supplier capacity.

For investors, especially a quantum-specialised fund like Firgun Ventures, the implication is that supply chain diligence should sit alongside technical diligence for hardware companies. Given the scaleup era is the focus, then the question is not only "can this modality win", but also "can this company reliably procure, qualify, and ship at volume under tightening controls and concentrated processing" and “what, if any contingency planning is in place”. That framing is consistent with Firgun's positioning as a quantum-first investor targeting the scaleup phase where commercial ambition has got to meet operational reality

Quantum advantage, the point at which quantum systems outperform classical ones on commercially and strategically relevant problems, will arrive. The question is not whether it happens, but who controls the infrastructure when it does. That question is, at its heart, a supply chain question.

Insights